Renee Ioannides | April 2 , 2026

The most common form of private credit is providing direct funding to a business. Often businesses require funding for a short period of time, therefore can be happy to pay an interest rate 3-5% higher than a bank would commonly loan to be able to access the funding right away.

Private credit includes a range of lending positions including senior secured debt, junior secured debt, asset-backed lending, project finance, mezzanine debt and other forms of unsecured debt. The lending exists across a wide range of underlying asset classes.

You can get attractive returns in private markets by being able to provide capital quickly, while banks and large institutions may be slower to work with.

Senior secured loans

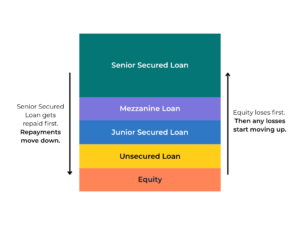

‘Senior’ means the highest ranked, the first to receive money in any event. By being at the top of the capital structure, you tend to get paid the lowest return if there are other more junior forms of debt in the capital stack.

A senior secured loan is the lowest risk form of debt from an investor’s perspective.

Typically in a senior secured situation, your security is over that company and all its assets and can be registered first on the Personal Property Securities Register (PPSR).

Junior loans

If a company already has a senior secured loan in place and wishes to access more debt, and the senior lender won’t provide more capital, the company will need to look elsewhere.

This would be an investor that is prepared to provide some debt funding on a less secured basis, such as a second ranking charge on the company. These investors are second in line behind the senior lender in the event of any problems with the company, which means they would expect to earn a higher return for taking on a higher risk position than the senior lender.

Unsecured loans

Unsecured loans sit below senior and junior loans, but above equity. If a company can’t acquire any more debt from its senior lender, it may source further debt through an unsecured loan.

Unsecured debt is riskier for the investor, given the subordinated position sitting behind other lenders, and because of this, the borrower usually pays a higher interest rate on the loan as it has less or no security.

Bridging finance

A type of unsecured loan, bridging finance is when you ‘bridge’ a short-term funding requirement for a corporate entity.

A company often approaches the private credit market, rather than the banks, in a short-term funding situation as the banks can take longer to approve the loan. If you require financing quickly, you tend to go to the private markets.

Debt plus warrants

When a business is in the early stages, such as seed or growth capital phase, and are requiring a senior secured loan as they are approaching profitability, the lender may require additional compensation for the risk to provide a loan. The company may not be able to afford the higher interest rate that would match the risk-return view for the lender. The solution to this can be for the company to add warrants (think call options) to the loan agreement.

This means the lender who provides the senior secured loan has the option to receive company equity at a fixed price later. This can make the lender comfortable that they are being appropriately compensated for the risk as they will potentially own part of the company in perpetuity, and if the company is successful the return could be significant for investors.

Asset-backed Lending

This type of private credit lending refers to the situation when you have a real asset or a portfolio of assets sitting behind the loan. These company assets include inventory, accounts receivables, equipment or property as collateral.

Asset-backed senior, junior and mezzanine debt

Within asset-backed lending, there are senior secured, mezzanine secured and junior secured loans all over the same pool of security.

The use behind these different types of loans is simply that they create different investable assets, depending on the risk profile of the investors. In private markets you have investors that want higher returns and higher risk.

A junior secured loan would sit above the equity of the business. This can be the first exposure of losses, with the highest interest rate.

Next is the mezzanine tranche, sitting in the middle.

The senior position, the last exposure of losses. This is the safest position therefore the lowest interest rate.

Offering investors the choice to invest across various parts of the capital stack can create a more efficient and lower average interest rate for the borrower, because tranching lowers the risk of the senior secured tranche to the point that investors are willing to receive a lower return.

The primary difference between public markets and alternatives (private markets) is that public investing markets have commonly been easier to access. iPartners is about making alternative assets, as easy to access as equities.

We turn something complex and structured and simplify it so investors are able to access these opportunities.

Please note private credit investments have a number of risks that are often unique including (but not limited to) illiquidity risk, credit risk, market risk, interest rate risk, legal risk, regulatory risk and tax risk. You should read the relevant disclosure document and the full list of risks in it before making any decision to invest.