Andrew Baume | April 14 , 2026

The RBA again raised rates in mid-March to 4.10%, with a split of 5-4 in the voting for the hike. The argument for an immediate hike was driven by the escalation of war in the Middle East. One senior market economist suggested that three further hikes were likely to combat the rampant spike in oil pricing, which will inevitably cause an inflation surge.

If cash rates do move towards 5% there is a real risk to the economy and one potential outcome could be higher unemployment and stressed consumers. This would inevitably cause an economic contraction, which would be very difficult for the government. Although credit spreads could stay under pressure in that scenario, they would remain a safe harbour in comparison to the likely path of the equity market.

Fiscal policy is already in focus as the Budget is due on 12 May. Hawkish central bank observers calling for multiple further policy increases are implying that government policy will not be helpful to cooling inflation pressures. If further rate hikes are the clear path the government will likely look to ease pressure on consumers (counteracting RBA policy). Confidence in fixed rate bond markets could remain shaky for some time.

Property pricing is always in focus and higher interest rates are usually negative for the sector. We saw in 2022 that input cost shocks can create very difficult conditions for developers and tends to put the brakes on new completions. Perversely, the completed residual stock cannot be replaced at the same price so may perform well. The key to property is around structuring multiple exit opportunities and avoiding segments that are highly rates exposed.

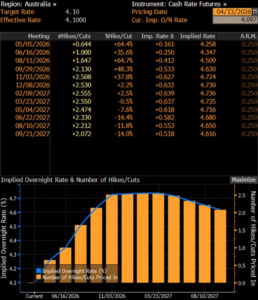

The chart from Bloomberg below shows the broader market’s expectations of interest rate moves over the next 18 months, with the cash rate expected to peak at 4.75% by the end of 2026.

Market commentary has been dominated by the likely outcomes of protracted Middle East conflict (which affects all asset classes in one form or another). While talks may never end, cease fires often do. The inflationary pulse pushed equities lower by around 10% but pricing in most regions remains considerably higher than a year ago. The key US S&P500 had recovered nearly all its March losses once the two-week ceasefire commenced. The prospect of higher interest rates has been shrugged aside, investors clearly seeing a difference from the inflation surge of 2022.

Private Credit has also had a constant raft of headlines with liquidity at its core. Most private credit investors understand that the segment includes an illiquidity premium so the action of funds protecting their unitholders by taking measures against forced selling of unimpaired assets should not be unexpected. The US market has a relatively high weighting to software related borrowers and nervousness about the effect of AI on that segment has pushed the boundaries of some portfolios’ natural self- liquidating properties.

Software companies are much rarer in Australian portfolios. Credit investing by its nature is a waiting game underpinned by confidence in approval and execution skills. Portfolios have loans maturing across the calendar with a new underwriting process accompanying any refinancing. Loan markets remain very competitive and core economic fundamentals particularly in Australia have kept default rates below or at long-term averages despite the blooming of the segment. Any withdrawal of capital to the sector in the short term is unlikely to have a material effect on borrowers who will likely respond by seeking more modest leverage, thereby reducing the return available to lenders.

Fund outflows in equity and credit markets do not exist in a vacuum. While money is taken to the sidelines in volatile periods there is still a need to generate returns for savers and superannuants. There has been a tremendous cyclical shift in recent decades as fewer workers globally are covered by company or government pension schemes and instead save for their own retirement. In the 2020’s there have been three negative shocks of note, the COVID period and the reversal of cheap money a couple of years later followed by the Liberation Day tariff announcement. Markets sold off significantly on each occasion, but the recoveries (particularly in the equity markets) were relatively quick and sustained.

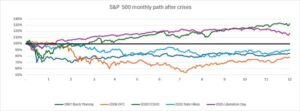

The chart from Bloomberg below shows the path of S&P returns the year after the 1987 crash, the GFC, COVID, the end of zero rate policy and last year’s Liberation Day tariff announcement. Recent market stumbles have either been far less deep or have resolved more quickly than past events.

Clearly there is a new investing paradigm. Workers are pre-funding their own retirement out of current earnings with regular and significant contributions which is having a profound effect. Although the current crisis may extend, markets have become much more resilient due to this liquidity effect. There is no sign of systemic frailties and investors who sit on the sidelines too long run the risk of not having money at work during recovery phases.