Travis Miller | April 22 , 2026

For many Australian investors, “property” evokes a familiar image: a suburban house with a backyard and a 30-year mortgage. While residential real estate is a cornerstone of national wealth, viewing property through the lens of an alternative investment opens the door to a diverse asset class. Property is capable of providing reliable returns, income stability, and a robust hedge against inflation.

The property asset class represents a sophisticated spectrum of risk and reward, understanding where you sit on this spectrum requires a deep dive into property sectors, capital structures, and the specific vehicles investors use to access them.

Property investment is generally categorised by the underlying utility of the land and buildings.

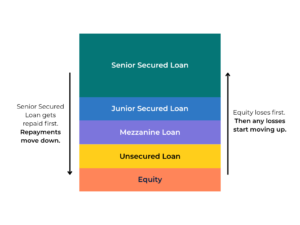

In any property transaction, there is a “capital stack.” Where you sit in the stack determines your priority for repayment and your level of risk.

The safest part of the stack. These lenders have the first claim on the asset if the borrower defaults.

These have no claim on the physical property. They rely entirely on the borrower’s cash flow or corporate guarantee, making them the highest-risk form of debt.

The capital structure can be seen visually below.

Equity represents ownership. However, the risk profile changes dramatically depending on the lifecycle of the asset.

This involves funding the construction of new assets. It offers the highest potential returns but carries significant delivery risk, including planning approvals, construction cost blowouts, and market absorption risk (that no one buys/rents the finished product).

Investing in a “de-risked,” tenanted asset, like a fully occupied shopping center or a childcare hub, is focused on yield. The primary risks here are vacancy (tenant default) and cap rate expansion (where the property value drops because market interest rates rise, making the yield return less attractive relative to other potential investments).

Please note private credit investments have a number of risks that are often unique including (but not limited to) illiquidity risk, credit risk, market risk, interest rate risk, legal risk, regulatory risk and tax risk. You should read the relevant disclosure document and the full list of risks in it before making any decision to invest.