Andrew Baume | July 16 , 2026

The RBA’s narrow path to achieving price stability without triggering a surge in unemployment meant no movement in interest rates in June. Alan Greenspan, the former Fed Chairman who died aged 100 last month, noted that there was a conundrum where the Central Bank cannot influence yields in the bond market. This has certainly been the case in Australia in 2026.

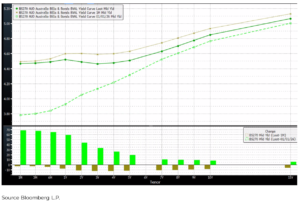

Australian yield curve in early July, early June and 1 January 2026

Throughout 2026, the yield on longer bond maturities has remained very stable despite 75 basis points of RBA rate hikes. Bond markets have offered far fewer opportunities for traders in recent years, with occasional massive repricing as occurred after the invasion of Ukraine in 2022.

Does the shape of the yield curve deliver us some predictive advice or is it simply a trader’s view? The bond market is a form of prediction market – traders get to trade on a fixed rate that is at its most basic a prediction for where the cash rate will be over a given period. The mathematics of the market can extract where it thinks rates will be at any time in the future.

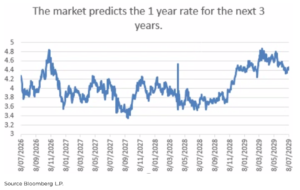

From the chart below we plot where the fixed rate market thought cash rates (represented by the 1-year interest rate) would be three years before it happened and also where the RBA cash rate actually was.

For most of the last 15 years the fixed rate market’s expectation of cash rates has been wrong. The margins of error are extremely high; failing to price in inflation risk when COVID was pushing rates to zero and misunderstanding the effects of globalisation on interest rates post the GFC. Each structural change persisted until the reality actually hit. The rates market is purely reactive, not predictive.

Looking back 18 months, we see the market at long last seems to have understood the economic conditions that now prevail. Has it got better at prediction, or has it been lucky? Recency bias occurs when recent events are more prominent that the overall picture. Cash rates started rising in Q2 2022 and once they rose have been in an historically narrow range for the last 3 years. The market predictions reflect that.

Where does the market think rates are headed?

If we are generous and say that the market has, after 15 years, got better at prediction we can take comfort in its predictions for the next three years.

This set of expectations calls for a “more of the same” path for Australian interest rates over the next three years. It is interesting that the market has never expected the 1-year rate to get above 5% and that boundary is both market driven but also a realisation that Australian borrowers (particularly homeowners) may struggle to afford the mortgage rates that cash rate would bring.

Australian borrowers are much more likely than Americans to have floating rate rather than fixed rate loans so despite the bond market doing little, the RBA is well aware that their actions have already had an impact on behaviour. The property market and consumer and business confidence are showing early signs of fatigue from rate hikes and unemployment levels are fluctuating. The weakness in the economy means the market is hedging its bets on even one further rate hike in this cycle.

Market Update

The consequences of the policy changes announced in the May budget are still working their way through the Australian economy. The more onerous conditions for residential housing investors (individuals and SMSFs) have added to the weakness that 3 rate rises had already brought to the housing market with auction clearance rates down to COVID era levels.

While it is too early to determine the longer-term effects, we believe commercial property is likely to be a relative beneficiary as capital seeks sectors less directly affected by policy intervention. We also expect completed residential stock to outperform development projects, benefiting from immediate cash flow, lower execution risk and reduced exposure to ongoing construction cost inflation.

The inflationary pulse is not limited to construction with fuel excise rebates finishing at the end of June and no definitive resolution to the Middle East conflict. The RBA will be forced to act if inflation gains another upward pulse, but it is increasingly likely that any further hikes will have a serious effect on economic activity.

Investment Landscape

Australia is a laggard in terms of equity performance in 2026 with the All Ordinaries only up low single figures for the year while most global indices are well into double figures. Our strong recent trade performance has unwound with higher cost oil imports combining with offshore sourced AI tools to push the balance back into deficit.

The USD has seen strength with the potential conclusion of the Middle East conflict seeing the AUD dropping to under .6900 having reached .7250 in early June. Historically these have been forerunners to domestic economic weakness; business and consumer confidence data is also painting a gloomy picture.

Notwithstanding these factors there is no doubt that remaining uninvested has been a weak strategy. Super Funds with their high levels of exposure to private markets have earned double digit returns this financial year, brushing aside sensationalist headlines and focusing on the long-term performance of their portfolio.

Market pricing is likely to remain volatile but there is little currently to suggest that borrower stress is elevated beyond normal intra cyclical levels.