Alex Thompson | April 2 , 2026

The term “stagflation” (stagnant economic growth, high unemployment, and persistent inflation) describes a confluence of factors that can be the ultimate bogeyman for investors. For Australian investors in 2026, geopolitical shocks and domestic fiscal pressures suggest the current environment may require a departure from the buy-and-hold portfolios of the last decade.

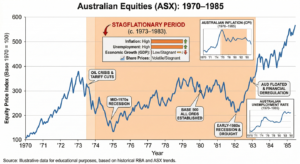

The last time Australia truly grappled with stagflation was the mid-1970s to early 1980s. Following the 1973 OPEC oil shock, Australia’s inflation peaked at nearly 18% in 1975, while GDP growth faltered.

Who were the winners?

– Real assets were the champions. Gold and commodities performed exceptionally well, acting as a store of value against a debased currency.

– Commercial property holdings with inflation-linked rent reviews also provided a partial hedge.

Who were the losers?

– Traditional bonds were decimated as rising yields crushed capital values.

– Equities (especially those without pricing power) struggled, as rising input costs ate into profit margins faster than companies could raise prices.

While the 1970s offer a roadmap, the current 2026 landscape features some unique pressures:

In this phase of the cycle, diversification into non-correlated assets is critical.

In stagflation, long-dated bonds (10+ years) are hazardous. As inflation expectations rise, the market demands higher yields, which causes the price of existing fixed-rate bonds to plummet.

Stagflation can be particularly concerning for certain corporate credit segments. Squeezed profit margins (from high input costs) and slowing consumer demand increase the risk of company defaults.

Has Australia fully crossed the threshold into stagflation in 2026? Investors should continue to monitor price persistence, growth stagnation and the labour market.

| Indicator | Most Recent Data | Period | Trend |

| CPI Inflation | 3.7% | Feb 2026 (Annual) | Remains stubbornly above the RBA’s 2–3% target range |

| GDP Growth | 2.6% | Dec 2025 (Annual) | Accelerating (from 2.1% in Q3 2025) |

| Unemployment | 4.3% | Feb 2026 | Increasing (from 4.1% in Jan) |

Source: Australian Bureau of Statistics (ABS) March 2026.

While 2.6% GDP growth appears healthy, the combination of rising unemployment and stubborn inflation suggests time for portfolio review. If the RBA maintains high rates to kill excess inflation, while the labour market continues to decay, the Bogeyman may settle in by year’s end.

As we move through 2026, the goal for most investors is no longer just growth, it is capital preservation and the search for real inflation-adjusted returns. Investors may want to reconsider passive indexing for defensive positioning. For fixed income investors this means moving away from vulnerable long-duration bonds and into FRNs and high-quality “essential” credit. By prioritising companies with the pricing power to outrun rising costs, investors ensure that while the Bogeyman may be at the door, he isn’t in your portfolio.