Andrew Baume | May 7 , 2026

The most recent rate hike cycle prior to 2026 was a violent move, driven by a combination of excessively low rates designed to be a safety net. COVID swept through economies and the supply side squeezed following the Russian invasion of Ukraine. Those who had sought what they expected to be the safety of the fixed rate bond markets saw the allocation that they had expected to be defensive losing as much as 20% in mark to market value. In early May, the RBA brought the cash rate back to the post COVID highs and the outlook for further hikes remains.

Most investors have a better understanding about the risk of investing in bonds in a higher yield environment, but the causes of this hiking cycle are still concerning. Stability within a portfolio of income assets is an important feature when markets are reacting to global volatility.

The extended conflict in the Middle East is driving up prices of oil globally with strong knock-on effects to other goods. In early May the price of crude has not settled but is trading a wide range, roughly 50% higher than late February. Consumer confidence in Australia has suffered a large drop and the RBA has already raised rates three times in 2026, completely erasing the cuts of 2025. This rate path actually started before the Iran conflict as inflation was shown not to be tamed and the speed of the hiking decisions has been endorsed by the rapid increase in inflation.

The market is predicting at least one further hike by year end and on the fence about a second. Although hikes increase costs in an already higher cost environment the RBA sees core inflation already well outside their target range at 3.3%. The Melbourne Institute Consumer Inflation Expectation is now 5.90%. that measure is the third highest in 25 years, just behind one period spikes after the GFC and the Russian invasion of Ukraine. The RBA had little choice but to move rates.

The path between too many rate hikes, (which causes a sharp contraction) and managing inflation expectations so we do not get to the 5.90% predicted by consumers, is a narrow one. The coming Federal Budget has the potential to be the most influential in many years, with many changes to policy expected. Whilst it is a difficult time to be a fixed rate bond holder, floating rate holders are benefitting from higher running yields.

US GDP remains on an upward trajectory despite geopolitical volatility. The massive investment in AI is now permeating the broader economy; notably, the median EPS for the S&P 500—excluding the distortion of Mega-Cap Tech—is projected to show mid-teen growth for Q1. This resilience is reflected in equity markets, which have climbed to all-time highs while largely dismissing fluctuations in oil prices.

While the Australian economy is lagging behind the US, this has yet to translate into fundamental weakness in the real economy. However, Australian credit spreads have widened due to localised inflation concerns—a sharp contrast to the rapidly recovering high-yield markets in the US and Europe. We see this as a strategic opportunity: investor pullbacks from debt allocations are driving enhanced returns, even as the underlying stability of most borrowers remains intact.

We are closely monitoring consumer lending arrears as a primary indicator of stress. While major banks have increased loan provisions, this is a standard response to uncertainty; notably, Westpac reported a decrease in stressed loans over the last six months. We expect fresh borrower behaviour data from S&P shortly. Furthermore, our tracking of public market securitisations in April will be critical in guiding our upcoming pricing and allocation strategies.

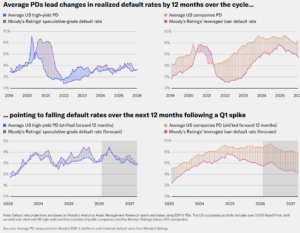

When the head of JP Morgan talked about private debt defaults being cockroaches and that once you see one there are probably more, he hadn’t disclosed that his firm had made more than USD 200 billion of loans to private debt lenders. Those advances are against tradable loans and mark to market fluctuations can be significant. According to the major rating agencies in the intervening 6 months default rates for High Yield debt remains under long term averages and is expected to remain so through 2026.

Most financial press has neglected to check in on the assertion to test how accurate the dire predictions of 6 months ago have been. Blue Owl, a manager that had been subject to numerous adverse headlines, has delivered much better than predicted portfolio outcomes and its share price has rallied more than 25% over the last month after a year of equity pressure.

There is no doubt that there are more under stress situations than there were over recent years, but those recent years were significantly lower than average. Moody’s show that historically their models are strong predictors of default frequency and they track the Probability of Default (“PD”) over time as well as defaults.

While JP Morgan’s recent warnings about leverage sent ripples through the US private credit market, the Australian environment remains a different beast. Local lenders rarely use the aggressive leverage seen overseas, and those who do keep it on a tight leash. The result? Very little systemic risk for local investors.

When the current “noise and bluster” eventually fade, the investors who stayed the course will likely see their portfolios doing exactly what they were designed to do: deliver steady, target returns. The hard data tells a much calmer story than the news cycle; those waiting on the sidelines may find that the biggest risk wasn’t the market itself, but the sub-optimal returns of sitting out.